Reviewed by Miyoung Won, M.D., FACOG

12 min read | TL;DR <1 min

Your clear, compassionate guide to aligning Social Security decisions with the life you want—in and beyond medicine.

TL;DR - Key Takeaways

- Big changes: WEP/GPO repeal is fully integrated (huge win for academic/VA physicians). 2026 wage base hits $184,500 (your S-Corp salary target). COLA increases benefits but Medicare premiums rise too.

- The math favors delay: Most physicians benefit from claiming at 70 due to longer life expectancy. The difference between claiming at 62 vs. 70 can exceed $600,000 in lifetime benefits.

- Watch the cliffs: IRMAA surcharges can add $2,000+/year for crossing income thresholds by just $1. Strategic planning matters.

- Action item: Check your projected benefit at SSA.gov and review your 2026 salary strategy if you're in private practice.

You've mastered complex diagnoses. You've guided patients through life-changing decisions. You've carried responsibilities that most people never face.

But when it comes to Social Security? Many physicians tell us it feels like starting over—unfamiliar rules, conflicting advice, and stakes that affect decades of your life.

We get it. And we're here to help.

This isn't about maximizing every last dollar. It's about making confident choices that support the life you actually want—more time with family, financial security, the freedom to practice on your terms (or step away when you're ready).

Let's walk through 2026 together with clear, practical guidance from people who understand the physician journey.

What's New in 2026? Key Changes Physicians Need to Know

Every year brings updates to Social Security. Some matter more than others. Here's what physicians planning their next chapter need to pay attention to in 2026.

2026 COLA: What It Means for You

The 2026 cost-of-living adjustment is 2.8%. For most retirees, that's about $56 more per month.

If you're a physician approaching maximum benefits at age 70, your monthly payment could climb from roughly $5,108 to around $5,251.

The catch? Medicare premiums often eat into this increase. The 2026 Part B premium is at $202.90—up from $185 in 2025. And if you're subject to IRMAA surcharges (more on this shortly), the math gets trickier.

The takeaway: COLA increases are real, but they don't happen in a vacuum. Keep an eye on Medicare costs too.

Delaying to 70 can add roughly $600,000 in lifetime benefits for many physicians.

The 2026 Wage Base: Your S-Corp Salary Target

The 2026 Social Security wage base is $184,500. (Up from $176,100 in 2025.)

If you're a private practice physician using an S-Corporation, this number matters. A lot.

Every dollar of W-2 salary up to $184,500 builds your Social Security benefit. Every dollar above that? It only triggers Medicare tax—without strengthening your future payments.

For 2026, if you're running an S-Corp:

- Set your W-2 salary near $184,500

- This maxes out your Social Security credits

- Anything beyond that? Take as distributions to save on payroll tax

It's a sweet spot—meeting IRS "reasonable compensation" standards while optimizing your long-term benefit.

Payment Schedule: When Benefits Arrive

Social Security payments in 2026 follow the usual pattern, based on your birthday:

- Born 1st–10th → Second Wednesday of the month

- Born 11th–20th → Third Wednesday

- Born 21st–31st → Fourth Wednesday

Small detail, but helpful when planning monthly cash flow.

Maximum Benefits: What "Full Optimization" Looks Like

Here's what maximum Social Security benefits look like in 2026, depending on when you claim:

| Claiming Age | 2026 Benefit | What This Means |

|---|---|---|

| Age 62 | ~$2,710 | Early claiming reduces your monthly benefit by about 30%. |

| Age 67 (FRA) | ~$4,152 | Your "full" benefit—no reductions or increases. |

| Age 70 (new claimants) | ~$5,181 | Delayed claiming adds 24% more than your full retirement age benefit. |

| Age 70 (with 2026 COLA) | ~$5,251 | If you claimed in 2025, your 2026 benefit reflects the COLA increase. |

Most physicians won't hit these exact numbers—but many come close. And the gap between claiming at 62 versus 70? That's nearly $30,000 per year. For life.

WEP/GPO Repeal: Finally, Full Benefits for Academic and VA Physicians

This is big news—especially if you've spent part of your career in academic medicine or with the VA.

The Social Security Fairness Act was signed into law on January 5, 2025. It permanently repealed both the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO), effective for benefits paid after December 2023.

Retroactive payments started rolling out in February 2025. By 2026, the repeal is fully baked in—no longer a "change," just reality.

The repeal removes a long-standing penalty that disproportionately affected academic physicians and VA clinicians whose earnings histories included years of non-covered service.

Who benefits most?

- Academic physicians at state universities (UC, UT, LSU, OSU, and others)

- VA physicians under FERS or CSRS

- Any physician who worked in "non-covered" employment (where Social Security tax wasn't withheld)

What this means:

- WEP increases averaging $300–$500/month

- GPO elimination restores full spousal and survivor benefits

WEP/GPO Repeal: A New Era for Academic Physicians

As of 2026, academic and public-sector physicians can receive their full Social Security benefits without WEP or GPO penalties. For many faculty and VA physicians, this is the most meaningful Social Security improvement of their entire career.

If you're in academic or VA medicine, this is one of the most important changes in decades. Time to recalculate your retirement projections with your full benefit intact.

How Your Training Years Shape Your Benefit

Physicians have an unusual earnings pattern. You start earning real income later than most professionals—often not until your 30s.

But once you do? Your income typically stays at or above the Social Security wage base for the rest of your career.

The "Lost Decade" During Training

Social Security calculates your benefit using your highest 35 years of earnings. For physicians, that often means:

- Ages 22–29: College and medical school (likely $0 in Social Security earnings)

- Ages 30–35: Residency and fellowship (modest earnings)

- Ages 36–70: Attending physician (high, consistent income)

Those early low-earning years? They definitely get factored in. But here's the good news: they hurt less than you'd think.

| AIME Range | Percentage Replaced | What This Means for Physicians |

|---|---|---|

| First ~$1,286 | 90% | This tier always gets filled, even with early zero years. |

| ~$1,286 to ~$7,749 | 32% | Most physicians fill this tier completely. |

| Above ~$7,749 | 15% | This is the only tier where those training years really matter. |

Bottom line: Even with a decade of low or zero earnings, most physicians still reach 80–85% of the theoretical maximum benefit. Your attending years carry you further than you might think.

Private Practice Physicians: The S-Corp Salary Strategy

If you run your practice through an S-Corporation, you face a yearly decision: How much should I pay myself in W-2 salary versus taking distributions?

It's a balance. The IRS wants you to pay yourself "reasonable compensation." Social Security only credits earnings up to the wage base. Getting this right matters—for your future benefit and your current tax bill.

| Salary Level | What Happens | Impact on You |

|---|---|---|

| Below ~$184,500 | You underfund Social Security | Lower lifetime benefits + higher IRS audit risk. |

| At ~$184,500 | You've hit the sweet spot | Maximum SS credits + meets IRS standards for reasonable comp. |

| Above ~$184,500 | You pay extra Medicare tax | No additional Social Security benefit—just more tax. |

Your 2026 S-Corp Salary Bullseye

You can edit text on your website by double clicking on a text box on your website. Alternatively, when you select a text box a settings menu will appear. your website by double clicking on a text box on your website. Alternatively, when you select a text box

For many private practice physicians, the 2026 wage base of ~$184,500 is the ideal W-2 salary target. It maximizes Social Security credits, supports "reasonable compensation" in an IRS audit, and avoids unnecessary payroll tax above the wage base.

Pay yourself too little:

- Your future Social Security benefit suffers

- IRS audit risk goes up (especially for high-revenue practices)

Pay yourself too much:

- You trigger more Medicare tax

- Without improving your Social Security benefit

The 2026 target: Align your W-2 salary with that $184,500 wage base. It's the cleanest way to maximize benefits while staying IRS-compliant.

Note: The IRS doesn’t care about ‘wage base optimization’—it cares that your S-Corp salary is reasonable compensation for the work you perform. For many physicians, that may land near the Social Security wage base, but it could be higher or lower. Work with a CPA to document why your salary level is reasonable before you engineer around the $184,500 cap.

Tax Planning: The Hidden Costs Physicians Often Miss

Social Security isn't just a benefit you receive. It's also taxable income. And for high-earning physician retirees, it interacts with Medicare in ways that create real financial surprises.

The Social Security Tax Question

For most physicians, 85% of your Social Security benefits will be taxable. The phase-in range (where benefits gradually become taxable) typically only affects lower-income retirees.

If you have pension income, investment income, or part-time consulting work in retirement, you'll likely pay tax on 85% of your Social Security from day one.

Why this matters: Social Security functions more like a taxable annuity than a tax-free benefit. Plan your retirement cash flow accordingly.

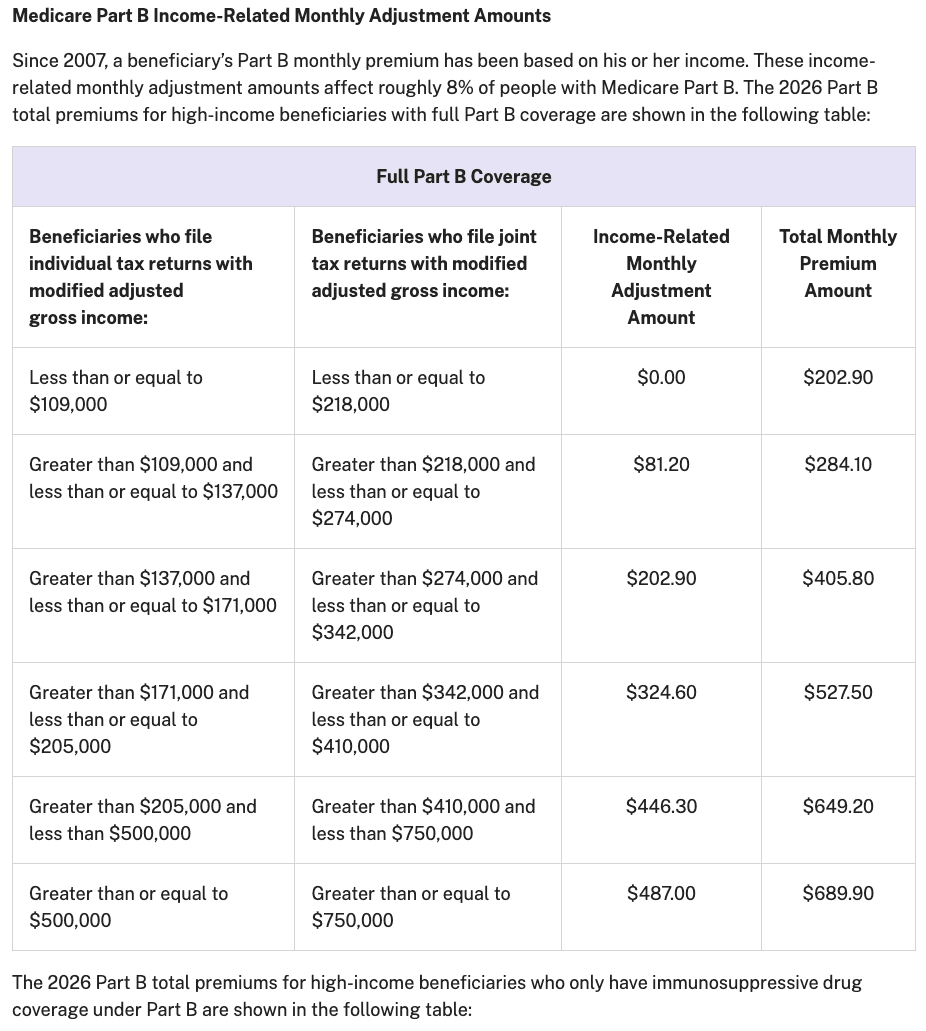

IRMAA: The Medicare Surcharge That Catches Physicians Off Guard

Income-Related Monthly Adjustment Amounts (IRMAA) are additional Medicare premiums charged to higher-income retirees. Unlike regular Medicare premiums that everyone pays, IRMAA is a surcharge added to Part B and Part D when your Modified Adjusted Gross Income (MAGI) exceeds certain thresholds.

These thresholds operate as "cliffs"—meaning that exceeding a tier by even one dollar triggers the full surcharge for the entire year.

Here are the IRMAA tiers for 2026 (source: 2026 Medicare Parts A & B Premiums and Deductibles)

Beware the IRMAA Cliff

Crossing an IRMAA tier by just one dollar can increase a physician couple's Medicare premiums by roughly $1,900–$2,000 per year. Thoughtful Roth conversion timing and careful MAGI management are essential in the years leading up to age 65.

The cliff effect: Notice how $1 over $218,000 adds nearly $2,000 per year for a married couple. This is why strategic income planning—Roth conversions, charitable giving, timing of capital gains—matters so much in retirement.

The two-year lookback: our 2026 IRMAA is based on your 2024 tax return. A large Roth conversion at age 63 can trigger higher IRMAA at age 65.

Strategies that help:

- Convert to Roth during your "golden window"—those early-retirement years when income dips

- Avoid jumping multiple IRMAA tiers unless the Roth math clearly supports it

- Use qualified charitable distributions (QCDs) after age 70½ to reduce MAGI

Your Longevity Advantage: Why It Changes Everything

Physicians tend to live longer than the general population—and this can have a profound effect on Social Security.

According to a recent analysis in JAMA Internal Medicine, physicians have substantially lower mortality rates than comparable non–health-care workers, especially among high earners, though the advantage is smaller—or even reversed—for some women and minority physicians. That doesn’t guarantee you’ll live longer, but it does mean planning as if you might need income into your late 80s (and beyond) is prudent.

While the average American may collect benefits for 15–18 years, some physicians will receive payments for 25–30 years or more. A physician couple where both live into their 90s could collect Social Security for over three decades.

This longevity advantage means physicians collect benefits for more years than the typical American retiree—turning Social Security into one of the most valuable "longevity insurance" assets in their portfolio.

When you're likely to collect benefits well into your nineties, every percentage point of increase from delayed claiming compounds over hundreds of monthly payments.

Delay to 70: The Math That Matters

When to claim Social Security is one of the biggest financial decisions in retirement. And for physicians—with your longevity advantage—the math tends to favor waiting.

Here's what the numbers look like:

A physician entitled to ~$4,152 at full retirement age (67) would receive:

- ~$2,710/month at age 62 (30% reduction)

- ~$5,181/month at age 70 (24% increase)

The difference? Nearly $2,500 per month. Or about $30,000 per year. For life.

Delay-to-70: A Powerful Lever

For long-living physicians, delaying Social Security from 62 to 70 can increase lifetime benefits by an estimated $500,000–$600,000, especially when paired with a well-funded 403(b), 401(k), or 457(b) bridge strategy.

For the early-retiring physician, the Bridge Strategy remains the most powerful financial maneuver available.

The Bridge Strategy: How to Retire Early and Still Delay Social Security

Most physicians retire around 65. But the optimal Social Security claiming age is often 70.

How do you fund those five years?

The Bridge Strategy works like this:

- Use 457(b) plans (penalty-free withdrawals at any age after separation from service)

- Tap taxable accounts or Roth IRA contributions (tax-free and penalty-free)

- Draw strategically from traditional IRAs/401(k)s to manage your MAGI

Using retirement accounts to "bridge" the gap—filling the income years between early retirement and age 70—allows you to delay claiming while maintaining lifestyle continuity. For many physicians, this creates the highest lifetime Social Security payout.

The strategy delivers:

- A larger lifetime Social Security benefit

- Smaller required minimum distributions (RMDs) later

- Lower lifetime IRMAA exposure

It's one of the most elegant moves in physician retirement planning.

Special Situations: Academic, VA, and Public-Sector Physicians

If you've spent part of your career in "non-covered" employment (where Social Security tax wasn't withheld), the WEP/GPO repeal is a game-changer.

Academic Physicians (UC, UT, LSU, OSU, and Others)

Many state universities don't participate in Social Security. Before 2025, this created severe WEP benefit reductions.

With WEP/GPO gone, everything's different:

- Mixed-career physicians now receive full Social Security benefits

- Consulting and moonlighting income becomes more rewarding

- Spousal strategies are fully restored

Next step: Verify whether your institution opted into Social Security. If not, you're now eligible for full benefits on any covered work—private practice, locums, consulting.

VA Physicians (FERS vs. CSRS)

CSRS physicians (hired before 1984): Your federal pension was never covered by Social Security. WEP used to reduce any outside SS benefits you earned. Not anymore.

FERS physicians (hired after 1984): Your federal employment is already covered. WEP never affected you—but if you have a non-covered pension from another job, the repeal still helps.

Older CSRS physicians benefit enormously from WEP/GPO repeal—especially those who moonlighted or worked locums during their VA career.

Key Takeaways for Physicians Planning Around 2026

Here's what matters most:

- Most physicians benefit from delaying Social Security to age 70—your longevity advantage makes the math work.

- The 2026 wage base of ~$184,500 should guide your S-Corp salary planning if you're in private practice.

- WEP/GPO repeal is fully integrated by 2026—a major win for academic and public-sector physicians.

- IRMAA surcharges can add $2,000+ per year for physician couples. Strategic MAGI management matters.

- The Bridge Strategy remains one of the highest-ROI approaches for early-retiring physicians.

Moving Forward: Your Next Steps

You've spent decades building a career that matters. You deserve a retirement strategy with the same level of care and precision.

Social Security isn't just a government program—it's a foundational income stream that, when optimized, supports decades of financial security and freedom.

Here's what's new and important in 2026:

- Full integration of WEP/GPO repeal

- A COLA increase

- Clear salary optimization targets for S-Corp physicians

- Better strategic clarity around IRMAA and Roth conversions

Small, real-life actions you can take this year:

- Set your 2026 S-Corp salary target to the $184,500 wage base

- Pull your 2024 tax return and estimate your 2026 IRMAA tier

- Run benefit projections at ages 62, 67, and 70 (you can do this at SSA.gov)

- Map out potential Roth conversion windows during low-income years

- Confirm whether your institution participates in Social Security (if you're academic or VA)

- Consider the delay-to-70 strategy paired with a Bridge approach

You don't have to figure this out alone. And you don't have to be perfect. Progress beats perfection every time.

If all you do this month is check your projected benefit at SSA.gov? That counts.

One step at a time. That's how we build the retirement you actually want.

Resources & Further Reading

- Social Security COLA Announcements — SSA

- How You Earn Social Security Credits — SSA

- AIME & Benefit Formula Explanation — SSA

- Early vs. Delayed Claiming Rules — SSA

- Maximum Taxable Earnings (Wage Base) — SSA

- Check Your Earnings Record — SSA MyAccount

- Medicare Premium & IRMAA Updates — CMS

- Social Security Fairness Act (WEP/GPO Repeal) — Congress.gov

- Physician Mortality & Longevity Studies — JAMA Network

- VA Physician Retirement Overview — VA.gov

Important Disclaimer

This article provides general educational information about Social Security planning for physicians and should not be construed as personalized financial, legal, or tax advice. Social Security rules are complex and subject to change. Individual circumstances vary significantly, and optimal strategies depend on factors including earnings history, age, marital status, health, other retirement income sources, and personal preferences. Before making any Social Security claiming decisions or implementing the strategies discussed, consult with qualified financial, tax, and legal professionals who can evaluate your specific situation. While we've made every effort to ensure accuracy, Social Security regulations and tax laws may change, and readers are responsible for verifying current rules and seeking professional guidance.